✏️ Bond interest rate risk examples

✏ Suppose you have two bonds, A and B. Both are selling for par and have the same time to maturity, but bond B has a higher coupon rate. If yields rise from 6% to 8%. What will happen to the price of the two bonds?

- both will fall, but we can’t tell which will fall more

- both will fall, but bond B will fall more

- both will fall, but bond A will fall more

- both will fall, but bond B will rise more

✔ Click here to view answer

From “6 Principles of Interest Rate Sensitivity.” Both of these facts are relevant:

- “Interest rate risk is inversely related to c”

- Bond B would have less interest rate sensitivity, so A will fall more.

- Price sensitivity is inversely related to YTM

- Bond B has a higher YTM, so bond B will have a lower interest rate sensitivity. This will also cause A to fall more. Both facts cause A to fall more. C is the correct answer.

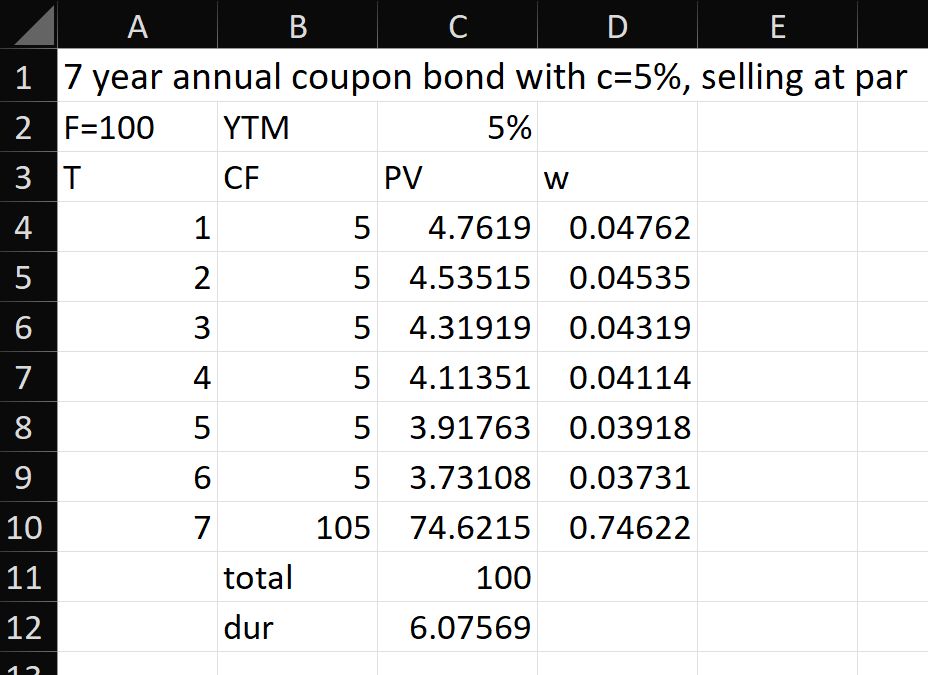

✏ Not a great exam question, but good for practice: Which will be more interest rate sensitive, a 5 year zero or a 7 year annual coupon bond with c=5%, selling at par?

✔ Click here to view answer

The duration of the zero will be five years because duration = maturity for a zero. What is the duration of the 7 year coupon bond?

The 7 year bond has a duration of 6.07 years. The 5 year zero has a duration of 5 years. The coupon bond has more interest rate risk.

✏️ Not a great exam question, but good for practice: Which will be more interest rate sensitive, a 8 year zero or Consol with a yield of 13%?

✔ Click here to view answer

Duration of the Zero is 8, as above. Duration of the consol is (1+y)/y = (1+13%)/13% = 8.6923 The consol has more interest rate risk.